In a recent webinar, “Become an SMSF millionaire” we run through the SMSF tax benefits.

SMSFs have a very low tax environment.

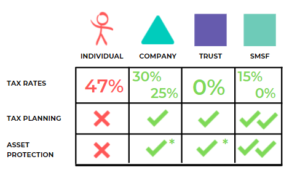

Under trust, it says 0% because trusts like discretionary trusts, give their profit to other entities or people in their family group and they pay the tax. 0% is not quite correct for trust but it actually gives it away.

With an SMSF, an SMSF pays 15% tax or 0% tax on the money it makes. So, they are much lower than the other tax rates and that is kind of a high-level overview of the differences between the tax rates.

Why are there two rates for an SMSF?

The first one is 15% when you’re accumulating your balance over the majority of your lifetime. Then you switch into 0% tax when you’re drawing a pension and when you are over a certain age. You can only get that 0% concessional rate on up to $1.7 million per member in pension. So, if you have $3 million in your own fund balance and in your member balance, then you can’t get that 0% concession on the whole lot.

On the difference. So, on the remaining $1.3 million, if you’ve got the total of $3 million in super, you will still pay the 15%. It’s still low and it’s just not zero. Even if you had $50 million in your own pension account, whatever it earns is taxed at 0%.

Benefits of drawing a pension or being in 0% tax mode plays out if you earn dividends from owning shares in super, then you will pay 0% tax. But some other instances are if you own a business through super, or part of a business, then the profits that go back to the SMSF in that pension account are at 0% tax and similarly if you sell an asset.

So what we see is if you buy a commercial property in your forties or fifties, hold it for 20 years and sell it when you are retired and in pension mode, you can make a massive gain and you can do that without paying any CGT.

Some of the things that you should consider in creating an SMSF strategy are:

Risks of your investments

If you’re investing in cryptocurrency, note that it might be extremely risky compared to leaving it in cash, which also has its risks with inflation. You need to basically have a common sense and documentation of the risks and why you’ve chosen that for each of the members.

Diversification of investments and benchmarks for classes of assets

You need to set in your investment strategy and you may target 60-70% of your fund that you want in real property whether it’s residential or commercial. You may want 40% in cash because you want a bit of liquidity, so you have to document what you’re aiming for and keep it up to date. Make sure the range that you are aiming for is what reality looks like.

If your SMSF holds property, and your home or property has increased in price and in value, then you may have a larger portion of your funding property and it may be on the upwards range of your investment strategy.

It is important to make sure that your investment strategy is kept up to date with the market values of your fund.

Document your intended return on investment

Document your intended return on investment and document your overall fund targeting the cash rate plus 5% or an overall return of 20% net of tax or whatever it is.

Borrowings

If you want to explore Borrowings in your fund, it is usually with property.

Insurances

It doesn’t mean you need to have insurance in your SMSF, but you do need to document what you’ve done with insurances.

Liquidity

Liquidity needs to be documented as well. It’s just common sense. There’s a bit of planning with liquidity and cash flow requirements. If you are in pension mode, you need to make an account for cash to pay out pensions. It’s not set and forget so we need to review that each year.

Need to speak to an accountant? Book a ZERO cost 20 minute strategy call with an Inspire Accountant at https://inspire.accountants/chat![]()

300K Gain Tax-Free Case Study

Tax-Free Case study:

A few years ago, we had a client who had a commercial property outside of Super worth about a million dollar value. He is shifting into retirement and he wanted to move more money and assets into Super. So, he transferred that million-dollar property to Super. He wasn’t an owner-occupier, but he received rent for a few years at 0% tax because he was in pension mode.

Within 2 to 3 years, he received an offer to buy that property for $1.3 million. And because he was retired, he paid no tax on the gains. So, he got a $300K gain at the 0% tax because he bought it for about 1 million, and sold it for 1.3 million – a great outcome for him.

Watch the full webinar, ‘Become an SMSF millionaire’ at https://learning.benwalker.com/courses/SMSFmillionaireweb

Here at Inspire, when there’s a couple in the family group, we designate one of them to be the risk-taker and one of them is the asset holder. And when we’re running the business, we are setting up structures for that family. When they are buying and investing in property or shares, we make sure it’s done very specifically.

Risk-taker roles are the director of the trading entities, the director of trustee companies if a trust is running the business. And ideally holds no assets in their own name. For instance, if the family home isn’t in their name.

In terms of the asset holder, they’ve got control of the assets and holding entities such as asset trust and bucket companies. 100% ownership of family assets like home, cars, and their typical roles in structures are the shareholders, trustee of asset trusts and the appointor of trusts.

What if the asset holder just buggers off and leaves the risk-taker without anything, nothing in their own names?

We’ve been told by multiple family lawyers that even though the assets are spread between the spouses with 100% in one and zero in the other, all of that is seen as marital assets. In the case of relationship breakdown or divorce, it’s not just one person who gets everything and the other gets zero. The idea of that is because the family court is the court that can look through all this asset protection and structuring.

Need to speak to an accountant? Book a ZERO cost 20 minute strategy call with an Inspire Accountant at https://inspire.business/chat

![]()