JobKeeper Eligibility Update

The ATO wants to make sure you have done some research from an eligibility perspective, documenting why you believe you are eligible.

The ATO have said that any attempts to defraud or fiddle with the numbers so that your business becomes eligible won’t be taken lightly and will take firm action if they believe you’ve done this.

On the other hand, let’s say you’re estimating your eligibility for the June quarter and instead of being 35% downturn, you’re only 28% downturn, the ATO will ask you to document why you estimated the original downturn and what happened to make it only 28%.

Now let’s say you turn out to be ineligible but close to eligibility (like the case of 28% downturn, not 30%). We’ve seen guidance that the ATO might consider your JobKeeper payments are ok to go through anyway. If you’ve legitimately tried to do the right thing and it happens that you have just missed out, so technically not eligible, they might let you keep the payments anyway. We’ll know more as the ATO releases guidance.

If you need help with JobKeeper book a strategy call with one of our accountants: https://calendly.com/inspireca/strategycall

How To Get The Best Out Of Your Team During COVID-19

I had the pleasure of joining Natasha Hawker on a webinar last week around the topic of JobKeeper. Natasha is an employee expert and founder of Employee Matters. Her biggest piece of advice right now is to communicate!

Here’s what she said –

This should be done on a frequent basis with empathy and care. We are going through something that we’ve never experienced before. Keep your team up to date in a dynamic and constantly changing environment. If you don’t know the answer, it’s okay to say, “I actually don’t know the answer.”

Make sure that everyone has a framework of the temporary and the new working environment. For example, you have an employee who has a JobKeeper direction, such as a change of duties, now they’re going to be doing some filing for you.

I would suggest the following framework to structure that conversation;

- Pinpoint exactly what you want them to accomplish;

- Create a measurement or some KPIs for monitoring progress to give them that qualitative and that quantitative feedback;

- Provide feedback, then reward and recognise them and;

- Keep checking in to find out how they’re going

And you never know, you might find out they really like what they’re doing in the new circumstances or they may find something in the process that you never knew, could be done better or see opportunities that you’re not seeing.

Communication is key. You have to massively increase the frequency of your conversation with your team. Just because they’re out of sight doesn’t mean they’re out of mind.

Natasha Hawker

https://www.natashahawker.com/

Employee Matters

https://www.employeematters.com.au/

https://www.facebook.com/Employeematters

https://www.linkedin.com/company/empl…

Listen Now! HR Hero Podcast

HR HeroesJobKeeper Scheme – Part 2 – analysis & the reality from a legal, accounting & HR

If you need help with JobKeeper book a strategy call with one of our accountants: https://calendly.com/inspireca/strategycall

Don’t Make This Big Mistake When you apply for JobKeeper

“If accountants are advising to add directors on the payroll, is it wise to get their instructions in writing?”

Here’s what we suggest. We received an email from the Tax Practitioners Board regarding the response to COVID-19 saying,

“Some advisers may be grappling with the tax consequences associated with the stimulus payment and wondering what will attract our attention. We also know that some businesses are already making changes to their business structures and employment arrangement following the stimulus announcements.

We ask that tax agents and businesses be mindful that it is not acceptable to backdate or artificially change your business structure or employment arrangements including changing the characteristics of payments in order to obtain a benefit or payment that would otherwise not have been paid. The Tax Practitioners Board and the ATO will take firm and swift action should this be the case.”

This email could not be more black and white. What is clear is that the ATO will come after you should you wish to change things in terms of your employment status on the payroll, changing from trusts to companies, or take your drawings as salaries.

The ATO can easily find this information by simply looking at the differences in your payroll this year versus last year. If the accountant is saying you can do it, that’s their own tax agent registration at risk. We advise a strong “no.”

If there is a downturn you are experiencing but not sure what you can receive in the JobKeeper payment, talk to an accountant who has read and been across everything JobKeeper. You don’t want to be caught in the crosshairs of the ATO.

If you need help with JobKeeper book a strategy call with one of our accountants: https://calendly.com/inspireca/strategycall

Monthly Reporting Requirements for JobKeeper

Each month, to receive the cash from JobKeeper, you need to claim the JobKeeper payment from the ATO business portal and report some key numbers.

You will need to go to BP.ATO.gov.au (Business Portal ATO) or your accountant can do it via their Tax Agent Portal and each month, report a couple of things:

The first one is your GST turnover of the previous month. April is the first full month we claim. Now that April has finished, you need to know what your GST turnover is. The ATO is also asking you for the estimate of the following month, or if you’re claiming for April, what is the month of May going to look like for your business. At the moment, we’re looking for the best guess of what May’s turnover will be. It doesn’t have to be exact and there’s no penalties if it’s way under or over. However, each month, you do need to report your actual turnover for the month just finished.

Secondly, what you also need to do is consider, “Are your eligible JobKeeper employees still eligible?” This is still relevant if you have any employees who leave employment (quit or terminate). So each month you’ll confirm the employees that you are claiming for and also confirm each fortnight you are claiming the payment for.

My recommendation is to lodge the monthly report as soon as you can.

We’ve already seen money starting to hit bank accounts for our clients. So as soon as the month finishes, in the first couple of days of the new month, make sure you get the reporting done. You will only receive the JobKeeper payments once these reports have been submitted.

If you need help with JobKeeper book a strategy call with one of our accountants: https://calendly.com/inspireca/strategycall

YFSB Interview

Owner and managing director of Wyntec – ideal technology solutions.

Married to Christy since 2001, 6 years old daughter, Arwin.

Started company in 2005, around the time of the GFC and had a 6 month old daughter. – ‘Insane, is the word I would use to describe it’

What was your reasoning to start up your company?

I went into it with an inkling that things could be done better in the area of IT – thats why I started my own business. I have come from a background of working in IT for 15 years for big corporates but…

my passion is to help and make things run better as well as just wanting to do something different.

My parents have always been small business owners, so it’s in the blood.

In simple terms, what do you do?

Stress free IT – I fix peoples computers and I take the pressure off people as IT frustrates the heck out of most people.

People rely on IT so heavily – the more they rely on it and the more it becomes supposedly intuitive the more frustrating it gets particularly when it doesn’t do what you want it to do. So we take the frustration off our customers by fixing their computers – we remove that stress!

What makes a good husband? / working for myself as apposed to working for a company…

My role is to be a provider.

The same principle for both family and business applies;

- be there,

- be available

- be flexible.

We share everything as she works full time too.

Why start your own small business?

The driving force for me in starting the business was about having flexibility. If I need to drop everything and go to my daughters ‘fathers day parade’ at school then I don’t have to worry about trying to get that time off work, I can just go.

family rhythms – school morning drop off is my thing with my daughter and then I’m always home before 6 for dinner and story time.

weekends are generally family.

I try to do more strategic things at night after my daughter has gone to bed as there are less distractions.

What is your one piece of advice to manage both worlds Business & Family?

Make time!

Lack of time is not an excuse… You don’t have to be available 24/7 for your clients, yes, you are your small business, but you can block it out even for 2 hrs a day. My 2 hours is spending time with my family over dinner and then get back to whatever needs to be done after but its about making time – Blocking it out in the calendar.

What is your business?

MyCladders does transportable buildings; colour bond roofing metal roofs, wall cladding

we put on roofs and gutters and help builders build roves.

What was your reasoning to start up your company?

I am accountable to myself. I have the ability to give someone a full time job.

What makes you a good husband?

It’s about the level of commitment between husband and wife. Find a balance between business and family. To be a good husband means to be well balanced.

What makes you a good father?

To be a good father it requires discipline with your child and selves as a married couple. We are the biggest role model in our son’s life. When you say you will do something you have to then follow through. If I’m not a good husband then I wont be a good father. It’s about discipline and balance of time.

What is your one piece of advice to manage both worlds Business & Family?

I personally try to switch off at 5pm from the business. now it’s family time, away from work time. The office is currently at home, it wont be for long, what’s hard with the office being at home is it is easy to get swept back into and it and it can continue. I need to switch off, having a designated time to switch off so i can contribute to the running of the house hold.

I look for the little wins with both family and business to bring balance, you really need this! It’s important to know how to switch off and to be fully present. Its a family soul business, that means

I bring a lot of the business into the family in relation to the people in the business are friends outside of the business. I make it really clear that Business is business and personal is personal. This helps them see that their boss is a human being and helps with the balance!

It’s ongoing. You cant be stand with your feet in concrete cause thats when it will all fall apart!

I started my own business in 2012 (3 years ago)

I left a much larger corporation owning 50% of the company to take the plunge.

Wife: Emma.

4 kids, (2 under 2years old). Isabella,Tate, Quinn, Enya

What is your business and what do you focus on?

Building and creative design- innovation for entertainment through Law.

The two things that differentiates us from other lawyers is speciality and focus – We focus on industry within the entertainment spectrum; musicians, film, builders of wealth, business- what drives them. We understand the way these people think, talk, breath, what makes them click. We focus specifically on, immigration of media, leaders within this field in the country.

What has been the biggest change going from corporate to small business?

Which is more stressful?

I am everything in my business.. You don’t have access to that administration, marketing director, 2 salary partner, grounds clerk when you run your own small business. In big companies there is plenty of leverage that can be done. The stress’s and pressures are different between each. It’s by no means easier in a small firm just different (every call’s mine, my balls are on the line, my kids eating is on the line.)

One of the things I notices is stamps are 60c. I am now licking my own stamps for the first time in years!.

When I was working in corporate Law I employed my wife to be part of the team and saw a huge turn around in the business. – It was hard having my wife work for me but it was the best decision as it helped me be able to transition out of that company cause it wasn’t the right fit for me. My wife then wanted to come over to help me with my new business and thats how it happened.

How are you a good husband?

To be a good husband honesty is the key.

We have worked out a routine that has been very helpful. Dad is the point of call when he is home from work.

My wife needs extra time support especially when it comes to feeding and when you have extra kids the kitchen isn’t always the cleanest every day. Its not as simple as hiring nanny’s especially when you are a start up, so to speak, or in a young business.

It’s about balancing the family, Being around to be with kids.

I take Bella to school 3 days a week and I am always home to put the kids to bed.

We are not a 9-5 office. Getting home is important so 1-2 days a week I work though the night to have flexibility with the other days.

It’s not about working for working sake but it all about making room to be able to be flexible!

What where some of the things you did to keep the business ticking while you had 2 kids under the age of 2 when you started your business?

The right staff – actively small.

Everyone says ‘we are growing’ but we measure our growth strategy by how many staples are in the office. It’s about having the right staff and being clear with the work that you are going to take on, so we don’t just take walk ins off the street. we focus on a particular industry.

We don’t just put people on as staff for the sake of it. I prefer to have a 3rd of the output in the business in keeping 100% of the quality over that period of time rather than having twice the output half the quality cause thats a short term look. it has an effect on the bottom line but its a choice that we make. We focus on quality through well thought out staff members. quality rather than quantity, getting things done well!

Bucket Companies: The least known and most underutilised strategy to save thousands in tax

“Use Bucket companies – tax tip of the week!”

I’d love to shed some light on what we call ‘Bucket Companies’, also called:

- Corporate Beneficiary

- Dump Company

- Family Vault

- Second Super

- And a few other creative ones!

Why this strategy is so critical, is because it can help cap your tax rate at 30%.

And as a quick refresher, as a sole trader you can pay up to 51% in tax (including the temporary budget repair levy).

Who is a Bucket Company strategy for?

Ideally:

- Business owners (or investors)

- Running their business or receiving income through a discretionary trust structure

- Not caught under the Personal Services Income (PSI) rules (if you don’t know what this is, hopefully the rules don’t apply, but you can read more on PSI here)

The idea of a bucket company is that they take ‘excess’ profits, after distributing a reasonable amount to the people within a family group.

Bucket Companies are incredibly useful

- For business owners who earn more than their cost of living, and want to build a nest egg for their family;

- When business owners are having big fluctuations in incomes between financial years as they can be used to make the tax bills more consistent; and

- For business owners coming up to retirement or selling their business, and no longer earning as much business income moving forward.

What are the tax benefits of using a Bucket Company?

If done right, Bucket Companies can generally save thousands of dollars in tax for a client, year on year.

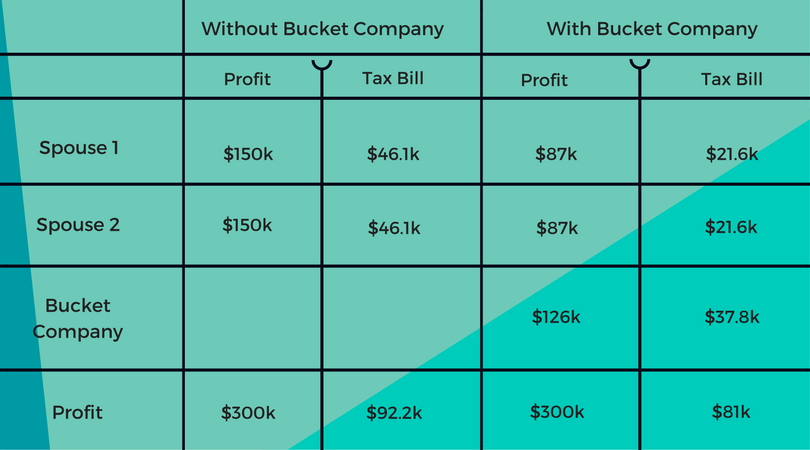

Let’s use an example of a trust earning $300k in profit. But we’ll review the tax rates first.

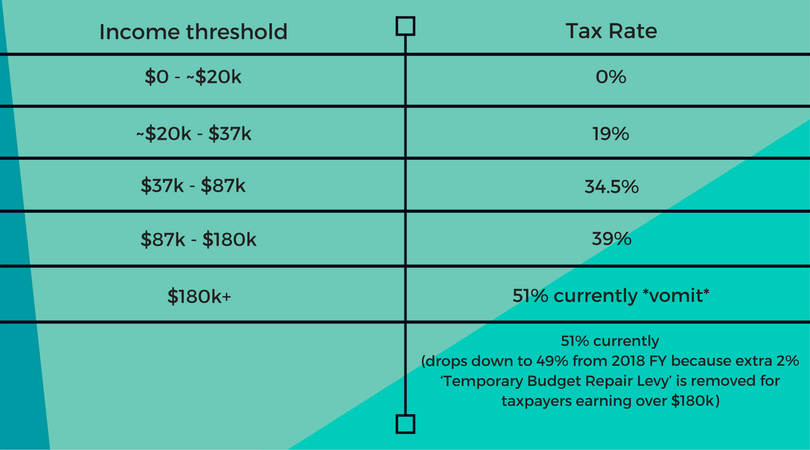

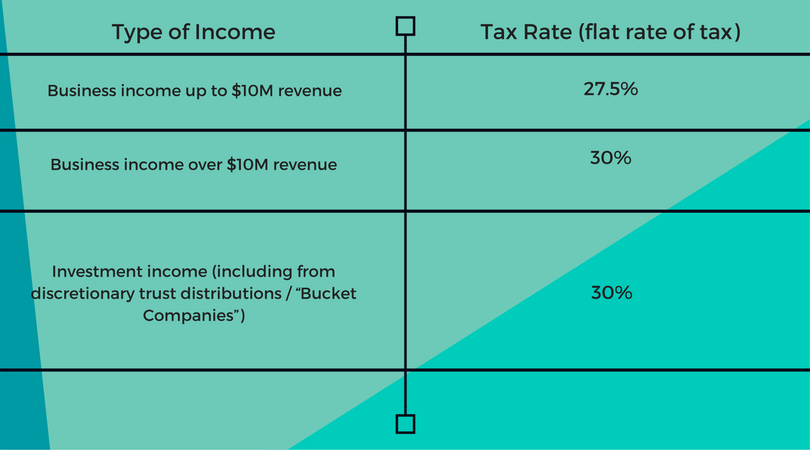

For 2017 FY, the individual tax rates (including medicare levy) are:

Company tax rates for 2017 FY are:

So if we’ve got a trust that’s earned $300k in profit, we need to allocate that to people or entities within a family group.

Now it makes sense to take eligible people up to $37k in income. That means we’ve taken them up to 19% tax on their income, and every dollar over $37k (but under $87k) they pay 34.5% tax. (See the table above)

Compare that to a company, where it would only pay 30% on the first dollar it receives, but every dollar after that.

But our ‘magic number’ from a distribution perspective to individuals (or people) is $87k, which might defy some people’s logic. This means they will be paying 34.5% tax on the income between $37-87k.

Do read on.

Do I need to actually pay the cash to the Bucket Company?

The reason why the magic number is $87k, is that when we distribute to a company, the cash needs to follow as well (the company needs to get paid). Otherwise we raise Division 7A issues and the ATO doesn’t like ‘on paper’ distributions without the intention of ever paying them.

We find that the $87k mark usually covers people’s cost of living, and they can commonly pay all or a good portion of the cash to their bucket company.

If you distribute to a company, then the company itself will have a tax bill. So you’ll have to pay at least 30% of whatever you distribute to it as a tax payment eventually!

What are the Tax Benefits of a Bucket Company?

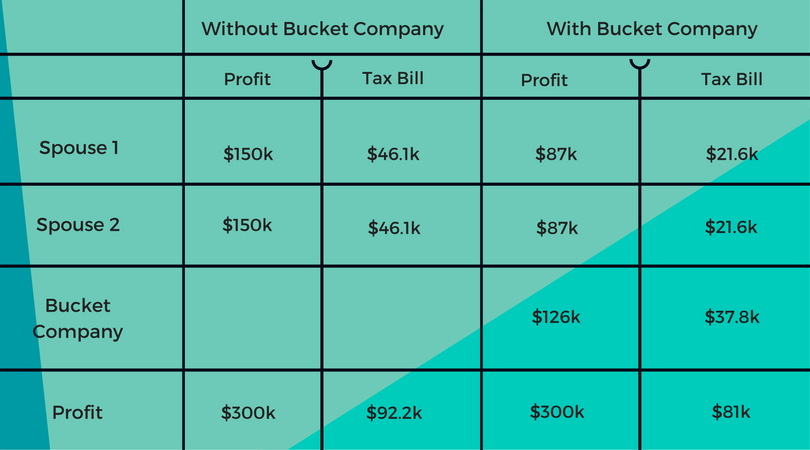

Let’s look at the benefits of the bucket company using $300k profit as a case study:

Tax saving by using Bucket Company $11,200. Not bad ‘ey?

Getting the cash out of Bucket Companies

We discovered above that the cash actually has to follow the distributed amount from the trust. And then the tax bill needs to be paid.

But now we’re left with some money in the company, so how do we get the money out?

Well there’s two ways to do it:

- Loan it from the company

- Pay dividends to the shareholders from the company

They both have their pro’s and con’s – let’s hit it:

1. Loan it from the company

These loans are called ‘Division 7A loans’ and are a minefield if not treated correctly, but can be used effectively.

Your Bucket Company effectively becomes a bank.

You loan money from it, and have to pay principal and interest repayments.

If your loan is unsecured, you have 7 years to pay back the cash.

If your loan is secured (on a property let’s say), then you have 30 years to pay back the cash.

The interest rate is set each financial year by the ATO, but usually not rediciulous. (5-7%)

So it’s kind of treating your company at arms length, like a bank, without dealing with the muppets.

This strategy can be very effective for loaning your 20% deposit for a house or property, then the 80% difference from an actual bank. That way (if secured) you get 30 years to pay back the loan to your own company. (More on this in a moment.)

2. Pay dividends to the shareholders from the company

The second way to get money out of a Bucket Company is through paying a dividend to the shareholders of the company.

The shareholders are who ‘own’ the shares in the company.

Now when we pay a dividend, the shareholders get taxed on that dividend, but they receive a ‘franking credit’ for the tax that the company has already paid.

Sidenote on franking credits: The company has paid 30% tax on their income, or 30 cents for each dollar it earned. When the company pays dividends, the shareholder is taxed on the full amount of the dividend (or profit the company has already paid tax on). But the franking credit offsets the tax bill for the shareholder. For instance, if the shareholder will pay on average 34.5% in tax on the dividend they receive, they get a 30% franking credit, only having to pay ‘top up tax’ of 4.5% on the dividend they received.

So you should always consider the tax impact of paying that dividend.

And MORE importantly, you must consider who the shareholders are of the Bucket Company.

If they are individuals, then you can only distribute to those individuals (in the % of shares that each of them own).

All too often we see husband & wife owning 50/50% of the bucket companies. But the problem with this is we may have little control on what the husband and wife earn separately to the dividend.

The best thing to own the shares in a Bucket Company is actually another, separate discretionary trust. We call these ‘Asset Trusts’.

That means when we pay the dividends from the company, they fall to the asset trust, then the trustees of the asset trust can allocate the didends to the family members who pay the least amount of tax. You retain ultimate flexibility.

In summary, getting the money out isn’t straightforward, and working with an advisor who knows their stuff is non-negotiable.

How will giving money to a Bucket Company affect my ability to get finance from a bank?

Stupid disclaimer and warning: always consult a savvy mortgage broker for questions about finance, aka a “Loans Guy or Girl”. Ben Walker isn’t a licenced credit representative, and this section is a compilation with Jake Pretorius from our office (our “Loans Guy”) and a licenced Credit Representative (No. 402028) of BLSSA Pty Ltd ACN 117 651 760 (Australian Credit Licence No. 391237). It’s based on our understanding of banks at the time, but they change their policies more then they change their underpants. Let’s keep in mind this is general advice and does not take into account your personal needs and financial situation.

Our understanding and experience with banks is that Bucket Companies don’t stop you getting finance from the banks.

Because you’re a business owner, the banks don’t just take your personal income to service your loan.

They’ll look at all related companies and trusts, and assuming there’s consistency, they’ll take your total group income into account.

So if you distribute $100k to a Bucket Company, banks should see this as your business income.

Can I use equity in my current property, plus cash from the Bucket Company for a deposit to buy an investment property?

While this is a complex question and scenario, but we believe it’s possible. But always check with your switched on mortgage broker to find the lenders who will do this.

Can the company buy property?

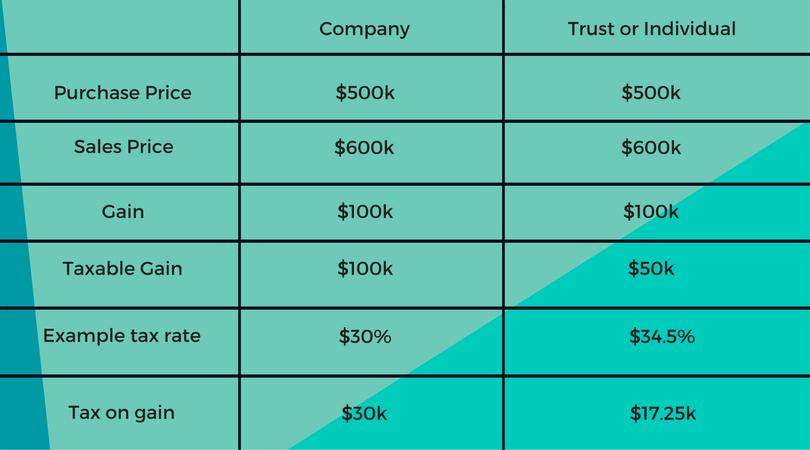

The company can technically own property and use the built up cash to buy it, but I wouldn’t recommend that strategy.

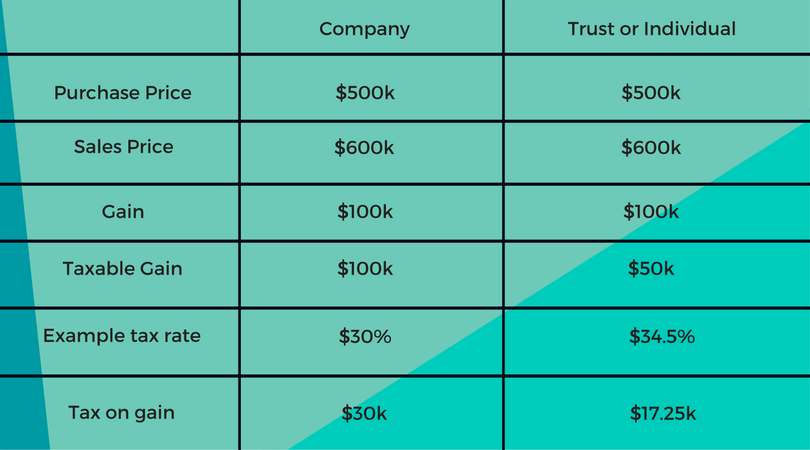

The simple reason why is that a company is NOT eligible for the ‘50% capital gains tax discount’, but a trust or an individual is.

Now in english, the ‘50% capital gains tax discount’ means that if you own an asset (like a property) for more than 12 months, then you get a 50% discount on the amount you get taxed on when you sell that asset and make a gain.

Some quick numbers on the benefits:

Tax saving by owning property in trust or individual is $12,750.

So to maintain ultimate control of your tax bill when you sell the property, own the property or asset through an Asset Trust.

Ok, so how do I use the cash in the company to buy property?

You can loan the money from the Bucket Company to your Asset Trust (secured). Then the rest can come from the bank.

This gives you 30 years to pay back the loan to the company, and assuming it’s an investment property, pay tax deductible interest from the Asset Trust back to your own Bucket Company.

See the “Loan it from the company” section above for more details.

And always, always, always see a switched on mortgage broker for help with this sort of loan structuring.

In conclusion…

That’s a super detailed overview of what we call ‘Bucket Companies’ and how you can use it to cap your tax rate at 30%.

If you want to ask any questions about this strategy or you’d like a second opinion on your tax, flick me an email to ben@inspireca.com.

Bucket Companies: The least known and most underutilised strategy to save thousands in tax

“Use Bucket companies – tax tip of the week!”

I’d love to shed some light on what we call ‘Bucket Companies’, also called:

- Corporate Beneficiary

- Dump Company

- Family Vault

- Second Super

- And a few other creative ones!

Why this strategy is so critical, is because it can help cap your tax rate at 30%.

And as a quick refresher, as a sole trader you can pay up to 51% in tax (including the temporary budget repair levy).

Who is a Bucket Company strategy for?

Ideally:

- Business owners (or investors)

- Running their business or receiving income through a discretionary trust structure

- Not caught under the Personal Services Income (PSI) rules (if you don’t know what this is, hopefully the rules don’t apply, but you can read more on PSI here)

The idea of a bucket company is that they take ‘excess’ profits, after distributing a reasonable amount to the people within a family group.

Bucket Companies are incredibly useful

- For business owners who earn more than their cost of living, and want to build a nest egg for their family;

- When business owners are having big fluctuations in incomes between financial years as they can be used to make the tax bills more consistent; and

- For business owners coming up to retirement or selling their business, and no longer earning as much business income moving forward.

What are the tax benefits of using a Bucket Company?

If done right, Bucket Companies can generally save thousands of dollars in tax for a client, year on year.

Let’s use an example of a trust earning $300k in profit. But we’ll review the tax rates first.

For 2017 FY, the individual tax rates (including medicare levy) are:

Company tax rates for 2017 FY are:

So if we’ve got a trust that’s earned $300k in profit, we need to allocate that to people or entities within a family group.

Now it makes sense to take eligible people up to $37k in income. That means we’ve taken them up to 19% tax on their income, and every dollar over $37k (but under $87k) they pay 34.5% tax. (See the table above)

Compare that to a company, where it would only pay 30% on the first dollar it receives, but every dollar after that.

But our ‘magic number’ from a distribution perspective to individuals (or people) is $87k, which might defy some people’s logic. This means they will be paying 34.5% tax on the income between $37-87k.

Do read on.

Do I need to actually pay the cash to the Bucket Company?

The reason why the magic number is $87k, is that when we distribute to a company, the cash needs to follow as well (the company needs to get paid). Otherwise we raise Division 7A issues and the ATO doesn’t like ‘on paper’ distributions without the intention of ever paying them.

We find that the $87k mark usually covers people’s cost of living, and they can commonly pay all or a good portion of the cash to their bucket company.

If you distribute to a company, then the company itself will have a tax bill. So you’ll have to pay at least 30% of whatever you distribute to it as a tax payment eventually!

What are the Tax Benefits of a Bucket Company?

Let’s look at the benefits of the bucket company using $300k profit as a case study:

Tax saving by using Bucket Company $11,200. Not bad ‘ey?

Getting the cash out of Bucket Companies

We discovered above that the cash actually has to follow the distributed amount from the trust. And then the tax bill needs to be paid.

But now we’re left with some money in the company, so how do we get the money out?

Well there’s two ways to do it:

- Loan it from the company

- Pay dividends to the shareholders from the company

They both have their pro’s and con’s – let’s hit it:

1. Loan it from the company

These loans are called ‘Division 7A loans’ and are a minefield if not treated correctly, but can be used effectively.

Your Bucket Company effectively becomes a bank.

You loan money from it, and have to pay principal and interest repayments.

If your loan is unsecured, you have 7 years to pay back the cash.

If your loan is secured (on a property let’s say), then you have 30 years to pay back the cash.

The interest rate is set each financial year by the ATO, but usually not rediciulous. (5-7%)

So it’s kind of treating your company at arms length, like a bank, without dealing with the muppets.

This strategy can be very effective for loaning your 20% deposit for a house or property, then the 80% difference from an actual bank. That way (if secured) you get 30 years to pay back the loan to your own company. (More on this in a moment.)

2. Pay dividends to the shareholders from the company

The second way to get money out of a Bucket Company is through paying a dividend to the shareholders of the company.

The shareholders are who ‘own’ the shares in the company.

Now when we pay a dividend, the shareholders get taxed on that dividend, but they receive a ‘franking credit’ for the tax that the company has already paid.

Sidenote on franking credits: The company has paid 30% tax on their income, or 30 cents for each dollar it earned. When the company pays dividends, the shareholder is taxed on the full amount of the dividend (or profit the company has already paid tax on). But the franking credit offsets the tax bill for the shareholder. For instance, if the shareholder will pay on average 34.5% in tax on the dividend they receive, they get a 30% franking credit, only having to pay ‘top up tax’ of 4.5% on the dividend they received.

So you should always consider the tax impact of paying that dividend.

And MORE importantly, you must consider who the shareholders are of the Bucket Company.

If they are individuals, then you can only distribute to those individuals (in the % of shares that each of them own).

All too often we see husband & wife owning 50/50% of the bucket companies. But the problem with this is we may have little control on what the husband and wife earn separately to the dividend.

The best thing to own the shares in a Bucket Company is actually another, separate discretionary trust. We call these ‘Asset Trusts’.

That means when we pay the dividends from the company, they fall to the asset trust, then the trustees of the asset trust can allocate the didends to the family members who pay the least amount of tax. You retain ultimate flexibility.

In summary, getting the money out isn’t straightforward, and working with an advisor who knows their stuff is non-negotiable.

How will giving money to a Bucket Company affect my ability to get finance from a bank?

Stupid disclaimer and warning: always consult a savvy mortgage broker for questions about finance, aka a “Loans Guy or Girl”. Ben Walker isn’t a licenced credit representative, and this section is a compilation with Jake Pretorius from our office (our “Loans Guy”) and a licenced Credit Representative (No. 402028) of BLSSA Pty Ltd ACN 117 651 760 (Australian Credit Licence No. 391237). It’s based on our understanding of banks at the time, but they change their policies more then they change their underpants. Let’s keep in mind this is general advice and does not take into account your personal needs and financial situation.

Our understanding and experience with banks is that Bucket Companies don’t stop you getting finance from the banks.

Because you’re a business owner, the banks don’t just take your personal income to service your loan.

They’ll look at all related companies and trusts, and assuming there’s consistency, they’ll take your total group income into account.

So if you distribute $100k to a Bucket Company, banks should see this as your business income.

Can I use equity in my current property, plus cash from the Bucket Company for a deposit to buy an investment property?

While this is a complex question and scenario, but we believe it’s possible. But always check with your switched on mortgage broker to find the lenders who will do this.

Can the company buy property?

The company can technically own property and use the built up cash to buy it, but I wouldn’t recommend that strategy.

The simple reason why is that a company is NOT eligible for the ‘50% capital gains tax discount’, but a trust or an individual is.

Now in english, the ‘50% capital gains tax discount’ means that if you own an asset (like a property) for more than 12 months, then you get a 50% discount on the amount you get taxed on when you sell that asset and make a gain.

Some quick numbers on the benefits:

Tax saving by owning property in trust or individual is $12,750.

So to maintain ultimate control of your tax bill when you sell the property, own the property or asset through an Asset Trust.

Ok, so how do I use the cash in the company to buy property?

You can loan the money from the Bucket Company to your Asset Trust (secured). Then the rest can come from the bank.

This gives you 30 years to pay back the loan to the company, and assuming it’s an investment property, pay tax deductible interest from the Asset Trust back to your own Bucket Company.

See the “Loan it from the company” section above for more details.

And always, always, always see a switched on mortgage broker for help with this sort of loan structuring.

In conclusion…

That’s a super detailed overview of what we call ‘Bucket Companies’ and how you can use it to cap your tax rate at 30%.

If you want to ask any questions about this strategy or you’d like a second opinion on your tax, flick me an email to ben@inspireca.com.

JobKeeper: Do I Need to Pay Super?

“Do I have to pay superannuation on the JobKeeper payments?”

There are three relatively common examples your team members might be in.

- Team members that have been stood down – not giving any hours to the business. You still need to pay the minimum $1,500 per fortnight to receive the JobKeeper payment for them. Any top-up amount or the full $1,500 is paid to an employee that has been stood down, there’s actually no super on that at all, which is great.

- Team member working part time or not on high wages (one or two days a week) receiving about $500 a fortnight. Keep in mind, you have to top up their pay to $1,500 a fortnight for you to be eligible for the JobKeeper payment. Let’s say, they’re working still and they’re earning $500. With the $500, that’s what you would normally pay super on. But any top-up amounts to take them up to the JobKeeper level, there’s no superannuation requirement on that portion, which is great.

- Team members paid more than $1,500 a fortnight – they’re still working for the business, they’re not stood down and they haven’t been terminated. Now, they’re already getting paid more than the minimum $1,500 per fortnight and if they’re working, then yes, you still have to pay superannuation on their salary or their wages.

So if they’re stood down, then no, you don’t have to pay super on the minimum JobKeeper payment.

If they’re earning something but not the full $1,500 and you have to top up their wage, you pay super just on what they’ve earned, not on that top up.

And if someone’s earning more than the JobKeeper and still working, then of course, no rules have changed there. There’s still superannuation on their salary.

If you need help with JobKeeper book a strategy call with one of our accountants: https://calendly.com/inspireca/strategycall